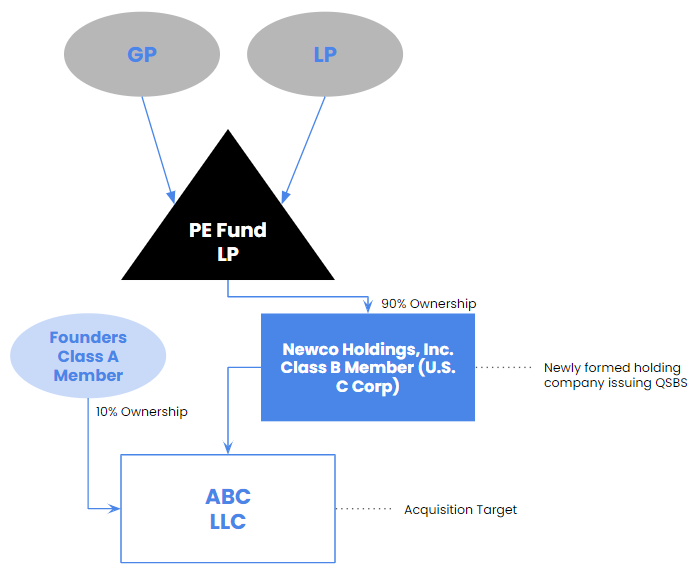

This scenario is a typical transaction structure that PE funds will utilize.

When a fund is acquiring a members interest in a pass through entity and not stock in a corporation the fund will set up a blocker corporation so that the income is not passing through to the fund, which can affect foreign or tax exempt investors.

This structure is done by forming a new holding corporation that will issue QSBS after the fund contributes capital to the holding corporation. The holding corporation will then acquire a controlling interest in the member’s equity of the LLC target company.

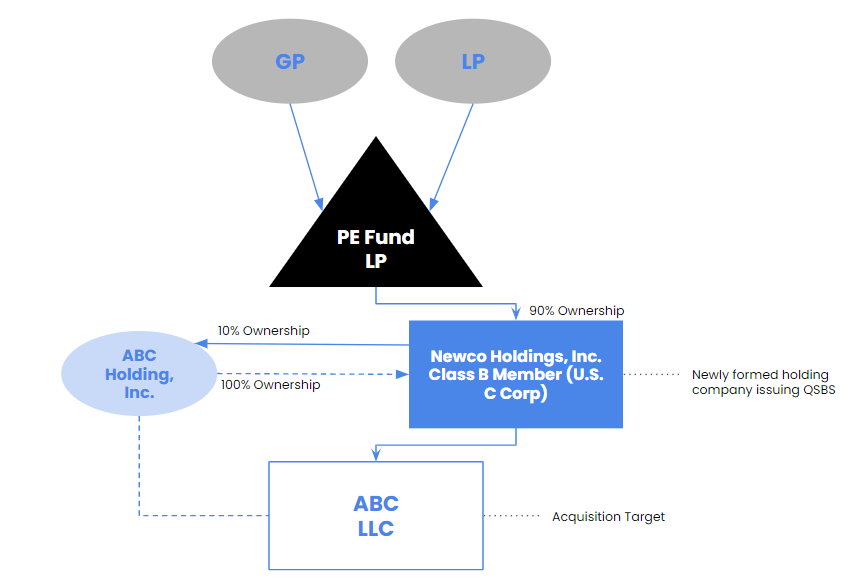

Tax-Free Member Interest Acquisition with Blocker Holding Company

The below scenario is a double tax saver in the fact that it takes advantage of (1) a Section 368 tax-free stock exchange and (2) a QSBS qualified transaction.

The PE fund will form a new holding corporation and contribute capital to the newly formed corporation for QSBS. Next the newly formed holding company will issue stock to ABC Holding, Inc. in exchange for 100% of the stock in ABC, Inc., which will be considered a Section 368 tax free transaction. Through ABC Holding, Inc. the Newco Holdings, Inc. will own 100% of ABC LLC. The aftermath of the transaction will be no realized gains to the shareholders of ABC Holding, Inc. and QSBS to both parties.

This article does not constitute legal or tax advice. Please consult with your legal or tax advisor with respect to your particular circumstance.